Policy Analysis: Repayment Under the PROSPER Act

Policy Analysis

An Example of Repayment under PROSPER Shows Students Will Pay More

In December 2017, the House Education and the Workforce Committee introduced its Higher Education Act reauthorization bill, known as the PROSPER Act. Under the bill’s proposed changes to the federal student loan program, graduate and professional borrowers are harmed the most.

The bill’s authors assert PROSPER’s reforms will simplify and improve student aid and that the proposals outlined will help students borrow responsibly.1 Those are certainly laudable goals, but the bill seems to miss two of the largest problems facing higher education today: maintaining access and increasing affordability. PROSPER would force many graduate and professional students into the private loan market, thereby severely limiting access to post-baccalaureate education. Additionally, as we illustrate below, repayment would become more complex to manage and more expensive than under current federal loan policies.

So, what would PROSPER’s student loan policies for graduate and professional students look like in the real world? Below we provide an example of a graduate/professional student to examine how repayment of her student loans would fare under PROSPER versus the current federal student loan program.

Loan Policy Differences

PROSPER eliminates the Direct Loan program (including Grad PLUS) in favor of a new “ONE Loan” program. Graduate ONE Loans would be capped at $28,500 per year with a $150,000 aggregate borrowing limit.2 Currently, graduate and professional students have access to federal unsubsidized loans and the Grad PLUS loan.3 The annual loan limit for the unsubsidized loan is $20,500 with an aggregate limit of $138,000.4 For Grad PLUS, the annual limit is primarily determined by an institution’s published ‘cost of attendance’ (COA), and there is no aggregate loan limit.

To repay federal loans, there are myriad options currently available, including income-driven repayment (IDR) plans, which allow borrowers to pay a percentage of their discretionary income rather than a predetermined fixed monthly payment. Under most of the IDR plans, a borrower can receive loan balance forgiveness after a certain number of years, typically 20 years or more. PROSPER offers two repayment plans: a standard 10-year amortized plan and an IDR plan in which one pays the amount one would have paid under the standard 10-year plan over some indeterminate time based on the borrower’s income. Neither plan offers loan balance forgiveness.

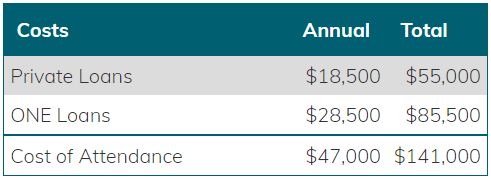

The bottom line is that under PROSPER, if the educational expenses5 of a program cost more than $28,500 per year, borrowers must find additional funding sources (likely a private education loan) to make up the difference. Moreover, the federal loans will have more borrower-friendly loan and repayment options; private loans likely will not.

To better illustrate this, let’s consider the example below.

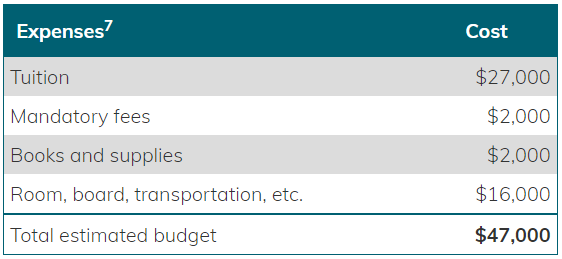

Assumptions and Expenses6

Assume Jane Doe got an advanced degree from a large, state school in the Midwest.8 She was a full-time student and her program lasted three years. She was also an in-state student for tuition purposes, and managed to live within her program’s suggested room, board, transportation, and other monthly expenses.9

Assume Jane Doe got an advanced degree from a large, state school in the Midwest.8 She was a full-time student and her program lasted three years. She was also an in-state student for tuition purposes, and managed to live within her program’s suggested room, board, transportation, and other monthly expenses.9

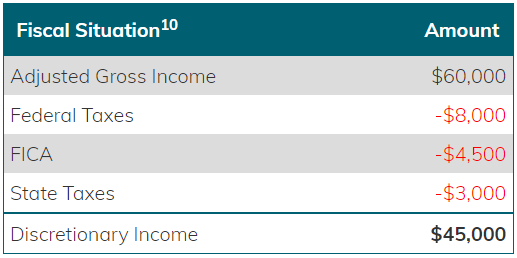

Also assume that Jane is a recent graduate earning an adjusted gross income of $60,000 per year. In this world, she is not married, has no children, and does not have other complex fiscal situations that would significantly reduce the amount of discretionary income she has available to repay her loans.11 In this scenario, she would have approximately $46,000 to use toward her expenses (e.g. rent, food, transportation, etc.).

The Loans12

At the end of Jane’s graduate or professional program, her student loan portfolio looks like this:

Because she had to borrow using both federal ONE Loans and private loans, she would have two different loan payments each month.13

Unaffordability

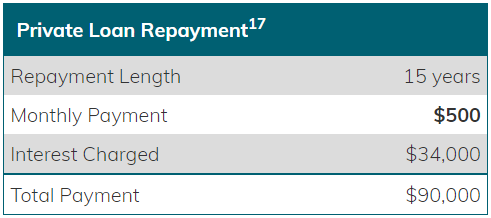

Under PROSPER, she would have two different loans that must be paid at the same time, thereby bringing her total monthly payment to over $1,000 per month before she even paid rent or bought food to eat. Given her salary, this combined monthly payment amounts to over 25% of her discretionary income, solely to pay off her student loans.

These numbers are remarkable given that the federal government’s current income-driven repayment program states that 10% of discretionary income is the target for borrowers to have manageable debt. Even the PROSPER Act sets its IDR payments at 15% of discretionary income.

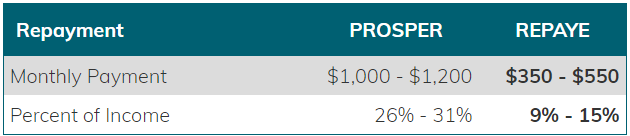

This lack of affordability under PROSPER is even more stark when one compares it to the most current repayment plan. Under the REPAYE program, borrowers pay 10% of discretionary income and receive forgiveness after 25 years. Here’s what Jane’s same loan scenario looks like under PROSPER versus REPAYE:

It is clear that repayment under PROSPER is significantly more expensive per month than REPAYE and other repayment programs. The current repayment policies allow borrowers to repay their student loans and manage their other financial responsibilities in a reasonable manner. This would not be the case for many graduate and professional borrowers under PROSPER.

At a time when students are struggling to pay off student debt, Congress should be reaching to make school and repayment more affordable, not less. The graduate student loan polices contained in PROSPER will only decrease access and make school more expensive for many students seeking to enhance skills by attending graduate or professional school.

While simplifying and streamlining the federal loan program are good ideas, Congress can craft better student loan polices for graduate and professional students - policies that ensure that students can both pay back their loans and not be burdened by crushing student loan debt.

1 House Education on the Workforce Committee. (2017). PROSPER Act Fact Sheet. Retrieved from: https://edworkforce.house.gov/uploadedfiles/fact_sheet.pdf. (this link no longer exists as it has been removed by the host site)

2 The annual and aggregate loan limits for certain medical programs are higher.

3 There are other loan programs graduate/professional students can utilize, but the vast majority of students who take out federal student loans use either an unsubsidized loan or a Grad PLUS loan. See AccessLex Institute and Urban Institute report, Financing Graduate and Professional Education: How Students Pay, (January 2018). Retrieved from: https://www.accesslex.org/resources/financing-grad-and-professional-education-how-students-pay. (this link no longer exists as the original article has been removed)

4 The unsubsidized aggregate loan limit for graduate students includes their undergraduate loans as well. This means the total loans available to borrowers under this program could be far less for graduate students if a borrower has already taken out undergraduate loans.

5 As articulated by an institutions’ COA, which includes tuition and fees, books and supplies, room and board, transportation, and other living expenses.

6 The scenario outlined is for illustrative purposes only. All calculations are based on a set of assumptions that can vary by individual. Borrowers should consult financial aid officers, specific servicers, financial institutions and the Department of Education for guidance on individual circumstances.

7 For ease of explanation, all figures used in this example are approximated by rounding to a thousand.

8 This example’s COA is based on a graduate program from a popular, large, state university in the mid-west. The tuition and fees figures are consistent with the average costs of graduate/professional school outlined in the AccessLex Institute and Urban Institute report, The Price of Graduate and Professional School: How much Students Pay, (June 2017). Retrieved from: https://www.accesslex.org/the-price-of-graduate-and-professional-school. (this link no longer exists as the original article has been removed)

9 While tuition, fees, and most other COA components are static among students, monthly living expenses can vary wildly based on geographic region of the country and individual circumstances.

10 All figures are approximations. Discretionary income will vary based on individual tax situations, including varying state and local taxes. In this example, tax figures were calculated using current 2017 federal tax law and an estimated state tax of 5 percent.

11 This scenario is constructed in a such a way to provide the borrower with the absolute maximum amount of discretionary income to repay her loans. Any additional life circumstances (e.g. children, spouse, etc.) would reduce the borrower’s income and thereby make repayment even less affordable and put the borrower in an even worse fiscal position.

12 All figures are rounded to the nearest hundred for simplicity.

13 The repayment calculations assume the borrower has two consolidated loans: federal and private.

14 PROSPER has a range of repayment amounts because they are based on a percentage (15%) of a borrower’s discretionary income. Repayment amounts will increase as a borrower’s income increases.

15 We assume the graduate receives a 1.5% annual cost-of-living increase in pay with no other source of reportable taxable income.

16 Based on current rates, we assume a 6.5% APR on a consolidated federal ONE Loan.

17 We assume comparable terms to the current federal loan terms by using a fixed interest rate consolidated loan with a 7% APR and a 15-year amortization.